Computable 100 | Best performing Software & IT companies in the Netherlands 2022

Private equity dominates Computable100 ranking through acquisitions

‘Add-ons’ drive further growth of businesses

CFI Netherlands’ top 100 is determined by the various financial results of Dutch IT companies. Participants may increase or decrease in ranking based on revenue growth, EBITDA margin, solvency and revenue per employee. The 2022 list was compiled based on the results of 2019, 2020 and 2021. It is remarkable that many companies are growing faster through acquisitions. The favourable economic climate and COVID-19 made a lot of capital available for acquisitions. Private equity backed companies, therefore, dominate the list.

CFI Netherlands annually compiles the financial list for the Computable 100. After compilation of this list, Computable interviews Ramon Schuitevoerder, Partner and Managing Director, and his colleague Randy de Visser, Vice President, to highlight certain IT developments. Higher profitability and improved solvency indicate that many parties have become healthier throughout the years. This year, further interpretation of the numbers proves more difficult as many IT companies are showing (significant) growth through add-on acquisitions. Private equity capital predominantly affects the ranking.

According to Ramon Schuitevoerder, this is understandable. The list is compiled based on a three-year average and in those years the COVID-19 virus had a significant impact on the results. COVID-19 caused a lot of economic uncertainty, however, many technology companies thrived during this period because of it. The low and sometimes negative interest rates on the capital markets in recent years suddenly resulted in much lower returns on investments for pension funds, insurance companies and other institutional investors, and in their search for yields they chose to allocate a larger amount of capital to much riskier private equity investments. Because of the success stories, the investors requested private equity to allocate an even larger share of committed capital to be invested in IT companies. The result: in 2020 and 2021, in particular, much more capital became available for acquisitions on the Dutch IT market.

Buy & Build strategy

Seven out of the top ten companies are backed by private equity and the others are two family-owned, and one listed company. Almost all of them show growth due to an active buy & build strategy. Seven IT companies are backed by private equity investors, six different investment companies are represented in the top ten. Mentha Capital appears twice with Aiden and Rapid Circle. According to Schuitevoerder it’s a positive development that there are so many IT acquisitions and that a lot of capital is being pumped into these businesses. Job growth, room for investments in technology and, ultimately, value creation. In addition, companies are increasingly important partners for customers and vendors. The share of capital invested in IT companies has grown in recent years, and as such there are more possibilities.

Financial market data

It continues to be a remarkable phenomenon that, in years where everything is laborious due to COVID-19, more capital is being pumped into private equity in general and more specifically into IT. In 2020 and 2021, Dutch and Belgian investors, who are active in the Dutch IT market, raised much more money than in the years prior. In 2020, roughly 6.2 billion euros was raised from institutional investors, while approximately 4 billion was already raised in 2021. In comparison, in 2018 and 2019, roughly 951 million and over 2.8 billion euros was raised, respectively. In 2022, the estimated amount dropped back to ‘normal’ levels of approximately 1.6 billion euros. In the Computable100 list, the average company revenues is 516 million euros reflecting an 11 percent growth over three years (and even an average one-year growth of nearly 32 percent).

Limited partners of private equity investors are mainly pension funds, insurance companies, wealthy families, and individuals. Private equity is normally perceived as a risky asset class, which is not always the preferred route as the capital is “locked up” for a certain number of years. If, however, other asset classes do not provide the desired returns, private equity becomes a serious option.

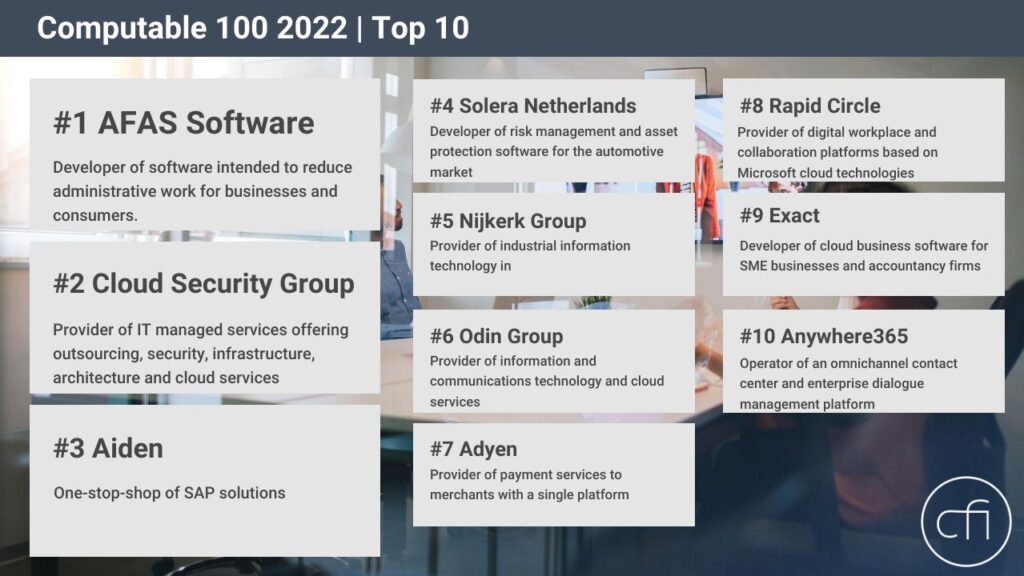

Afas Software

Afas Software, a family business, is back at the top of the list. Last year, it was suddenly surpassed by Anywhere365 and the Cloud Security Group. The story is not very different than in previous years: sticky customer base, large in SME, good product suite and high client lock-in. Afas provides a full ecosystem for many SME organisations.

Afas did well in 2021 due to implemented price increases and cross- and upselling of multiple modules and features. In addition, they were able to expand its existing customer base. The annual report shows that Afas has, once again, experienced strong growth in the Netherlands. Roughly 800 new customers were added to the existing base in 2021, predominantly smaller clients as sales processes for larger customers are longer. Smaller companies had to start working remotely and organise their workspaces accordingly.

Cloud Security Group

The Cloud Security Group is doing just as well as last year and is again in second place. The group is growing through acquisitions, with TIIN Capital being the financial sponsor. Lantech and Felton were acquired and merged in 2020. New management was appointed to start scaling up the organisation. They started to integrate before building the organisation. They began with looking for synergies between the two companies and how to cross- and upsell.

The sticky managed services contracts and the high margins on projects are the main drivers of Cloud Security Group. The company also provides cloud infrastructures to run software applications, which was positively affected by COVID-19 too as the demand for hybrid structures arose. Many companies suddenly needed to migrate to the cloud, without very complicated implementations. That’s what the Cloud Security Group is good at; scalable infrastructures and packages that do not require excessive customisation. Security is showing a similar wave in recent years, as security suppliers are not easily switched.

Aiden

Aiden is perfecting the podium with a third position in the Computable100. Last year it was ranked 5th on the list under its former name Xperi /Serac. In 2021, both companies merged with Asecom, Insynq, Meridian IT and ITvisors and rebranded into Aiden. Aiden is a buy & build platform in SAP technology backed by Mentha Capital as a financial sponsor.

Schuitevoerder notes that the SAP ecosystem is making a comeback and is the largest and most important European software company that can compete with Big Tech from the United States. SAP is also starting to make a name in the mid-market, which is the exact spot of Aiden. Aiden will also start exploring foreign countries and will follow customers abroad, providing people international career prospects which enhances the sourcing of consultants. The SAP market in Germany is significantly larger compared to the Netherlands, where the middle market is dominated by Microsoft. Germany is a straggler in cloud adoption where a lot of infrastructures are still on-premise, providing ample room to grow. Aiden is still mainly Dutch-oriented, but a move abroad, in particular to Germany in the short term, seems like a logical next step.

Solera & Nijkerk Groep

In fourth place, one of the largest software vendors for the automotive sector: Solera, a US player whose Dutch practice participates in the Computable100. The company provides different applications, from analysis and ERP software for the automotive industry, to very specific vehicle tracking, vehicle data and vehicle lifecycle software. The automotive vertical software market is a very sticky business. Solera is well positioned in a conservative sector and has an active buy-and-build strategy. They serve a multiple of verticals within the automotive sector and are organised in four business units with a multitude of on-top-of-packages. They have about 300,000 customers worldwide.

An old acquaintance with a new story ranks fifth, Nijkerk Groep which is known for when Vosko was still part of the group. Vosko was acquired by Conscia in 2017, after which Nijkerk Groep dropped on the list due to the impact it had on its financials. The current position is mainly fuelled by the financial consolidation of Silta and Frontforce, resulting in a revenue increase of approx. 8.5 million euros. An additional revenue increase of 2.2 million euros can be attributed to companies in France and Belgium. The effect of the Vosko acquisition has disappeared from the results. In 2018, 2019 and 2020, the Nijkerk Groep experienced a dip due to the sale of Vosko, but the financials are now back on track and growing once more.

Odin Group & Adyen

On place six is the Odin Group. This cloud service provider carries out projects and has its own data center. Private equity plays a major role at Odin and the company was backed by Fortino Capital Partners until early 2022, when it sold its stake to Apax Partners. Odin is growing fast, mainly organically, but also through acquisitions, such as Platani (2020) and Pimarox (2021). The group realises a nice growth in revenues, but an even bigger growth in EBITDA. They have also made a step up in their solvency. At the end of the investment horizon there is less debt on the balance sheet due to repayments in previous years, which improves solvency and reduces risk. Cash can be used for growth without going to the banks for additional financing. Fortino financed part of the transaction with debt, subsequently increased shareholder value in order to sell Odin on to Apax. They will play the same game on a bigger scale.

The same story as last year applies to Adyen, which was extensively discussed in last year’s Computable100. Adyen has grown enormously in e-commerce transactions due to COVID-19 and this growth has continued.

Other companies top ten

With Rapid Circle, Exact and Anywhere365 the top ten is complete. Rapid Circle is the second player in the top ten of investor Mentha Capital. Aiden focuses on the SAP ecosystem, while Rapid Circle is a player in the Microsoft ecosystem, focusing on Azure infrastructures. Rapid Circle also made several acquisitions in 2021, including Portiva in the Netherlands. With representation in the Netherlands, Australia, and India, it achieves a follow-the-sun strategy to serve customers in all time zones.

With Exact on place nine, there is another buy-and-build story. In this case, Apax Partners sold its stake to KKR, meanwhile Silver Lake Partners also entered as an investor. Exact plays the same game as Afas: a sticky business in SMEs and accounting software for specific vertical markets. Exact has made quite a few acquisitions, all of them fit into its buy & build strategy. More acquisitions in 2022 by Exact were noted, which will have their impact on next year’s list. In addition, Exact made their first acquisition outside the Benelux after divesting its international activities in the past.

Anywhere365 closes the top ten with a loss of nine places compared to last year. Anywhere365 suddenly was number one last year. In the beginning of the pandemic, Anywhere365 grew very fast, mainly due to the accelerated adoption of Microsoft Teams driven by the lockdowns and by working remotely. Anywhere365 is still growing, but at a “normal” pace.

Add-on investments

CFI sees a tilt in the market in which more add-on acquisitions are made. The acquisitions are getting smaller and are being added to existing platform investments. Fewer major platform investments have been made, so acquisitions are mainly driven by active buy & build strategies.

Add-on acquisitions are intended to accelerate growth inorganically. In recent years, huge amounts of capital have been raised by private equity parties in the Netherlands. That capital should now be put to work and add-on acquisitions are easier to finance than platform investments.

Supply chain-optimalisation

CFI also identifies four IT developments that will determine the Computable100 in the coming years. Supply chain technology and optimisation constitute the first trend as there is an increasing demand for transport management systems and supply chain management tools. Currently, the world is dealing with tremendous supply chain issues caused by shortage of raw materials, rising prices, geopolitical issues which drives inflation sky-high. Huge investments are made in supply chain optimisation in order to become more efficient. The aim is to make the supply chain more transparent to avoid wasting time and goods and to become more competitive.

The supply chain market is very fragmented. There are many suppliers in the supply chain, each focusing on one particular good or service. There are many suppliers in the chain that need to be monitored and reviewed. The buy-and-build platforms will focus on niche players in the market. Many international players act in these fields and it remains to be seen when this will have an impact on the Computable100.

Hyper automation & RPA

Hyper and Robotic Process Automation (RPA) is an emerging technology. Many rules can be automated, in particular in combination with artificial intelligence that can make recommendations. There are many adjacent domains which can be automated to a high degree. It’s all about increasing efficiency, reducing the use of people by using software, reducing costs, et cetera.

There is no particular party that will claim this domain, it is likely that the technology will be embedded in products, services and organisations. Parties surfing along this trend will grow faster. One example is ilionx, the biggest riser in the Computable100, which acquired You-Get. Data science and AI are the cornerstones of RPA. Every ecosystem and every vendor is going to embed this technology in its software suites.

Application performance monitoring (APM)

The next development: application performance monitoring in combination with infrastructure and cyber security. Due to COVID-19 a lot of parties had to migrate to cloud, which is attractive to cybercriminals. The entire ecosystem has to change and especially application monitoring. More companies will specialise in monitoring the domains of applications and application chains.

Odin, Total Specific Hosting, Broad Horizon and Sentia (that acquired Ymor, for example) are parties that are investing in application performance monitoring. They want to offer an all-in-one solution. Monitoring services and workplace management are key in this offering. For example, Total Specific Hosting, which acquired Eshgro and Sentia was sold to Accenture in 2022. Solvinity acquired an American cybersecurity provider, Securify, which was a technology play and not a footprint in the United States. Consolidation towards the cloud is continuing and customers like having a single point of contact for all IT-related matters.

Industry-cloud platforms

A last development that is emerging in the market is cloud platforms for specific industries. More software is being developed for very specific niches in the market. It concerns both applications as well as infrastructure which are being offered as an all-in one vertical solution. This can exist of CRM, but also ERP or the previously mentioned specific software. SAP provider Aiden specialises towards certain verticals such as retail, business services and manufacturing. Special functionalities and features are being developed for these verticals, increasing client lock-in and reducing churn. In addition, the Microsoft ecosystem with for example 9altitudes, HSO, Eshgro or Fellowmind are all focusing on specific possibilities and different areas of expertise.

Key is to offer a very specific discipline in a very specific industry or vertical based on a certain technology. These types of companies have great added value because they bring along sector expertise. Companies that are embedded and integrated at clients are hard to replace and ensure a certain lock-in. The customer simply can no longer ignore you. Organic growth is then mainly driven by adding new functionalities and modules. Companies can acquire complementary technologies, functionalities or modules, but they can also choose to build these themselves. If building them takes too much time, they will look for acquisitions, a build or buy matrix.

If you would like to know more about our experience in the Software & IT Services sector, then please do not hesitate to contact Ramon Schuitevoerder or Randy de Visser.