Benelux HR Tech M&A market update 2021-2025 H1: from fragmentation to consolidation

IN COLLABORATION WITH RECRUITMENT TECH

The HR Tech market in the Benelux is experiencing rapid acceleration. For many companies, investments in software, hardware, tools, and platforms that support the digitalisation, automation, and optimisation of HR processes and talent management are increasingly high on the strategic agenda. Driven by structural trends such as labour shortages and the ongoing digitalisation of HR, demand for innovative HR technologies has surged in recent years.

This strong growth has led to a significant increase in the number of HR Tech companies across the Benelux, most of which offer a new (often AI-driven) point solution or vertical application. As a result, the market has become more fragmented, creating ample room for consolidation, scaling, and the rollout of buy-and-build strategies. Both strategic buyers and financial investors are actively seeking acquisitions that strengthen their technology, functionality, geographic coverage, and market position. Consequently, M&A activity has grown strongly in the Benelux.

In this article, we share insights into the latest developments in M&A within the Benelux HR Tech sector. Drawing on Corporate Finance International’s extensive transaction experience in this sector and our active dialogue with key market participants, we provide a sharp perspective on the most important trends, drivers, and priorities among HR Tech players. We will take a closer look at the role of consolidating platforms, the key factors driving valuations, and conclude with an analysis of recent transactions and an outlook for the years ahead.

1. Market structure

Introduction

The HR Tech market in the Benelux is rapidly maturing into a well-developed ecosystem, fuelled by structural trends such as labour shortages, hybrid working, digitalisation, AI, demographic shifts, and evolving regulation (including ESG and GDPR). These developments are driving strong demand for advanced HR solutions that go beyond traditional HR information systems.

Market developments

M&A activity in the Benelux HR Tech space can be characterised by three themes:

- Fragmentation & Consolidation: the market is highly fragmented, particularly in niches such as recruitment, learning & development, talent management, and employee engagement. This fragmentation has triggered a wave of consolidation, with investors deploying buy-and-build strategies to unlock scale benefits, technological synergies, and commercial opportunities (such as cross-selling). Examples of consolidating platforms include Reducate and BCS.

- Platformisation: larger players such as Visma and Zvoove are building integrated HR solutions, while specialised providers continue to focus on targeted niches, such as AI-driven recruitment tools. The market is seeing both horizontal expansion (e.g. from recruitment into onboarding and payroll) and vertical integration (deepening workflow automation and process integration).

- Internationalisation: the Benelux is increasingly viewed as a strategic launchpad for pan-European expansion through buy-and-build strategies, as illustrated by US-based Bullhorn. The region’s high digitalisation rate and fragmented structure make it attractive for multiple targeted acquisitions, unlike more consolidated markets where acquisition opportunities are scarcer and competition is greater.

Market segmentation

As noted, the HR Tech market in the Benelux is fragmented, comprising a handful of large platforms alongside many smaller, specialised players. These specialists provide deep expertise within one of the following sub-segments:

- Recruitment

- Performance & talent management

- Learning & Development

- Compensation & Benefits

- HR analytics & workforce planning

- Employee engagement & wellbeing

- HR suite

2. Buyers

Platforms and buyer groups

The segmentation outlined above provides fertile ground for M&A activity, attracting both strategic buyers and financial investors:

- Strategic buyers typically focus on acquisitions that strengthen or broaden their existing offering, with the aim of enhancing their competitive position. A good example is SD Worx, which recently expanded its portfolio through acquisitions of Intelligo, Pointlogic HR, and Adesso.

- Financial investors tend to concentrate on scalability, growth potential, and opportunities for operational optimisation. For instance, Main Capital has built a strong portfolio of HR Tech companies, including BCS and TMA, which are being rapidly scaled through active buy-and-build strategies. Fortino Capital has also positioned itself prominently in the sector, with investments in Techwolf, Kaizo, and Peers.

Most active buyers

The HR Tech market in the Benelux has evolved from a collection of innovative software companies into a layered ecosystem of integrated platforms and international groups, often backed by well-capitalised private equity investors.

A notable example is Visma, which, under the ownership of Hg Capital, has completed no fewer than 16 HR Tech acquisitions since 2006, nine of which in the Benelux since 2021. Other highly active consolidators include Zvoove (13), Bullhorn (11), SD Worx (9), and BCS (8).

| Platform | Investor | Country | Vintage year | HR Tech add-ons |

| Visma | Hg Capital | NO | 2006 | 16 |

| Pixid | Keensight Capital | FR | 2015 | 4 |

| MySolution | Nedvest | NL | 2016 | 3 |

| Zvoove | LEA Partners | DE | 2019 | 13 |

| Bullhorn | Stone Point Capital | US | 2020 | 11 |

| BCS | Main Capital | NL | 2022 | 8 |

| Paragin | Main Capital | NL | 2022 | 3 |

| Archipel | Pride Capital | NL | 2022 | 4 |

| ISH Group | Strada Partners | BE | 2023 | 5 |

| SD Worx | WorxInvest, CVC | BE | 2023 | 9 |

| Lepaya | Meerdere | NL | 2023 | 4 |

| Reducate | All Seas Capital | NL | 2024 | 7 |

| Vitec | Beursgenoteerd | SE | n.a. | 2 |

| Salta Group | Privé | NL | n.a. | 2 |

Key valuation drivers for buyers

Although each company has unique characteristics influencing valuation, several general factors are of fundamental importance when assessing the value of HR Tech businesses:

| Factor | Explanation |

| Recurring revenue | Predictable revenue streams, forming the basis of SaaS models |

| Rule of 40 | Sum of recurring revenue growth (%) and EBITDA margin (%) |

| Scalability | Potential for efficient growth |

| Net revenue retention | Retaining clients (ideally with upsell) is key to growth |

| Churn | Customer attrition (% lost customers or lost revenue) |

| Market position & differentiation | Competitive advantage |

| Technology | Modern tech-stack, proprietary IP and scalability |

| CAC to LTV ratio | Customer acquisition costs versus customer lifetime value |

| Client concentration | Higher risk if overly dependent on a few large customers |

| Management team | Strategic vision, leadership quality, and execution capability |

| Contract structure | Longer contract terms reduce the risk profile |

| Exit potential | Ability to achieve a successful sale within 3-7 years |

A further key consideration is whether an acquisition qualifies as a platform investment or an add-on. Platform investments usually involve larger businesses with a proven business model, product-market fit, and scalability. These typically command higher valuation multiples due to their established market position and strategic relevance. Add-ons, by contrast, are usually smaller, complementary businesses. While multiples ultimately depend on synergies and growth opportunities, add-ons generally trade at lower multiples, partly reflecting their higher risk profile compared to platforms.

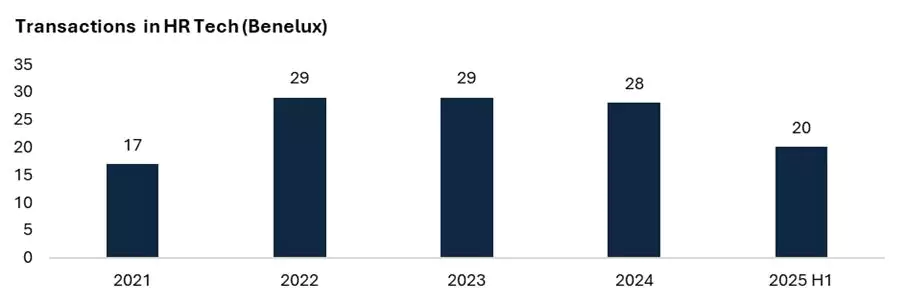

3. HR Tech transactions 2021-2025 H1

General trends

In recent years, the HR Tech market has undergone a wave of rapid consolidation. Companies active across a wide range of niches – from recruitment and selection to e-learning and employee engagement – have been integrated into larger ecosystems. This is reflected in transaction data, which shows a consistently high number of deals during 2022–2024. With 20 acquisitions already completed in the first half of 2025, deal activity is on track to surpass previous years.

Several factors are driving this momentum:

- Abundant but selective capital: Investors continue to hold substantial dry powder, while HR Tech offers a highly attractive combination of strong growth potential and solid fundamentals (i.e. high levels of recurring revenue and mission-critical services). In addition, HR software aligns closely with boardroom priorities, as talent retention and the adoption of AI in HR processes remain high on management agendas. This continues to fuel investor appetite.

- Sales readiness: Both strategics and investors are showing strong interest in mature, integrated HR platforms. The more comprehensive the offering, the stronger the equity story. Many of the businesses acquired by investors between 2019–2023 are now progressing towards platform maturity, with add-ons forming an integral part of this development.

- Buy-and-build proof of concept: Investors have demonstrated that HR Tech is particularly well-suited to add-on driven growth. These success stories continue to attract new capital inflows.

Geographic distribution of transactions

While the Benelux has long been recognised as a digital and innovative HR Tech region, M&A activity remained largely locally driven until 2023. In 2024, however, there was a sharp increase in cross-border acquisitions by international buyers, driven by three key dynamics:

- Many acquisitive European and US HR Tech platforms were established between 2017 and 2020. Having initially focused on domestic consolidation, these groups are now increasingly pursuing international expansion.

- Due to the COVID-19 pandemic, many companies postponed internationalisation until 2022, concentrating instead on familiar markets during that period.

- The “mid-tier” of Benelux HR Tech companies – those with several million euros in revenue and proven product-market fit – is particularly attractive for international buyers seeking immediate, substantial presence in a new geography. The intensive wave of acquisitions in 2024 was concentrated in this segment, resulting in exceptionally high deal volumes. It is therefore unsurprising that 2025 shows a temporary decline, as many of the most attractive targets in this category have already been acquired. This slowdown is expected to be short-lived, as the continued growth of smaller HR Tech businesses will generate new acquisition opportunities.

| Period | Benelux transactions | International buyers | International targets |

| 2021 | 8 | 7 | 2 |

| 2022 | 19 | 6 | 4 |

| 2023 | 19 | 8 | 2 |

| 2024 | 9 | 15 | 4 |

| 2025 H1 | 13 | 5 | 2 |

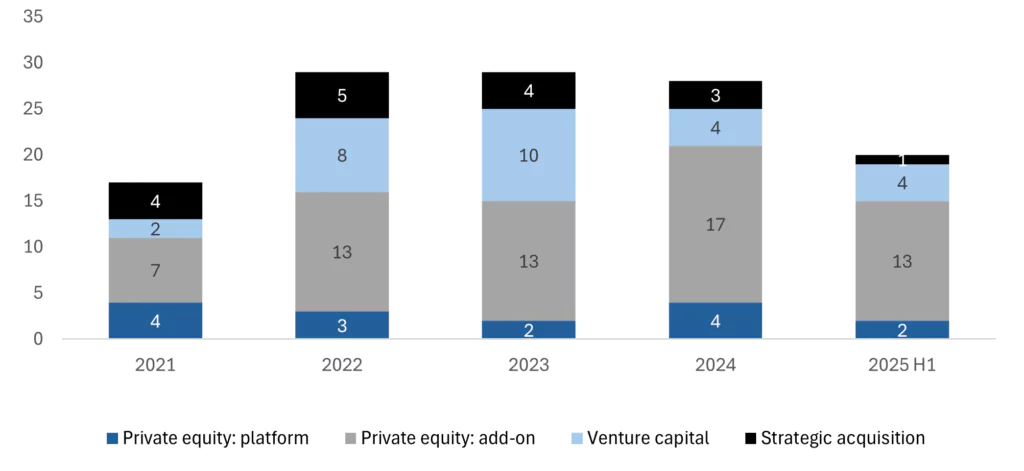

Transaction types (2021-2025 H1)

Recent years have seen a sharp increase in the number of add-on acquisitions by existing platforms. Key drivers include:

- High fragmentation: many relatively small and recently established independent HR Tech companies remain in the market.

- Cross-sell potential: HR Tech is increasingly marketed as an integrated proposition.

- Operational synergies: cost bases do not scale proportionately with revenue, e.g. through combined back-office and sales activities.

- Exit valuation uplift: larger, integrated platforms typically command higher exit multiples.

Another notable development has been the surge in venture capital funding in 2022 and 2023, followed by a decline in 2024. The COVID-19 pandemic accelerated the digitalisation of HR processes, attracting significant early-stage VC investment. At the same time, VC funding slowed during 2020–2021 due to uncertainty, which was subsequently offset by heightened activity in 2022–2023.

4. Expectations for 2025 and beyond

The HR Tech M&A market in the Benelux is expected to remain highly dynamic in the coming years, underpinned by several fundamental trends. Organisations are placing growing emphasis on the integration of AI, automation of HR processes, and the enhancement of the overall employee experience. At the same time, the pace of technological change is making in-house development increasingly complex. These dynamics continue to create attractive opportunities for both entrepreneurs and potential acquirers.

Strategic buyers are likely to focus on acquisitions that enable them to broaden their product portfolios, enter new markets, leverage innovative technologies, and realise operational efficiencies and cost synergies. Investors will remain drawn to the fragmented nature of the Benelux HR Tech landscape, providing capital to businesses with significant growth and scaling potential. In doing so, they will continue to play a central role in driving further consolidation and international expansion, accelerating the transformation of the sector both nationally and across Europe.

Recommendations

For most entrepreneurs, selling a business is not an everyday activity, making thorough preparation essential. The following recommendations provide practical guidance:

- Be aware of market dynamics and investment climate: Market conditions, interest rates, and the availability of capital have a direct impact on valuations and the likelihood of a successful transaction.

- Internal timing: A sale process is time-intensive and requires significant management attention. Choosing the right moment is therefore critical.

- Transaction rationale: A (partial) sale can be driven by multiple objectives. Having a defined rationale significantly accelerates and strengthens the sale process.

Interested in learning more about developments in HR Tech?

Would you like to discuss this article or the latest developments in the HR Tech market? Feel free to reach out to Kasper Kooij or Ramon Schuitevoerder for further insights.